Written By: Steve Waller | July 11, 2026

Time to Read 14 Minutes

What if the "expensive" loan you have been avoiding is actually the fastest way to scale your portfolio in 2026? Many investors watch lucrative deals slip away while waiting for traditional bank approvals that never come. It's frustrating to lose a property because of rigid debt-to-income ratios or slow-moving underwriters. You might feel that private hard money lenders are a "last resort" reserved for desperate situations. That's a common misconception that keeps many talented investors from reaching their full potential.

We understand the hesitation. You want transparent funding without the fear of hidden fees or confusing ARV vs. LTV calculations. This article will stop these misconceptions from stalling your next deal. You'll learn the truth about how modern private lenders actually operate as tactical equity partners. We're debunking five major myths for the 2026 market, covering everything from the latest FinCEN regulatory updates to the real cost of capital. It's time to turn hard money into your most powerful growth tool.

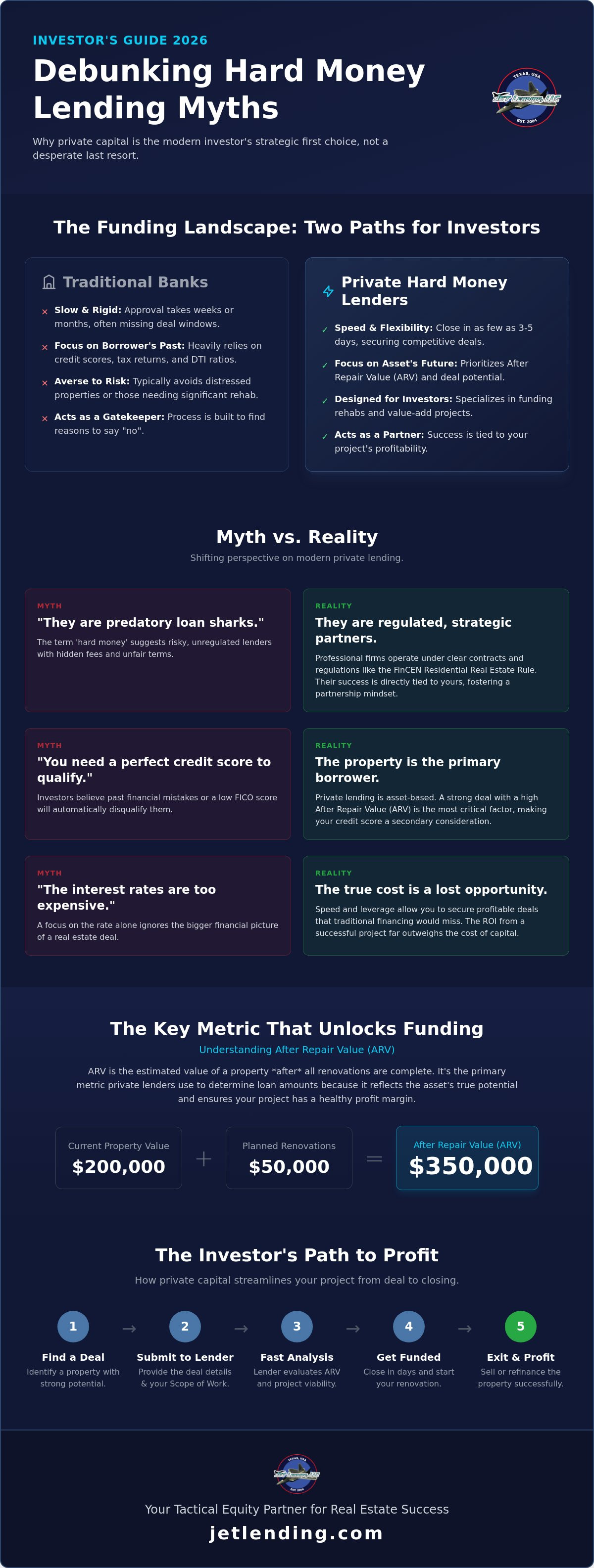

The term "hard money" often conjures up images of shadowy figures and predatory terms. This outdated stereotype couldn't be further from the truth in 2026. A Hard money loan is simply a short-term, asset-based financing tool secured by real estate. For savvy Houston investors, private hard money lenders have shifted from being a "last resort" to a strategic "first choice." Speed and flexibility win deals that traditional banks simply can't touch. You aren't begging for a loan; you're securing a tactical partner.

While "country club" lenders (individuals lending their personal cash) still exist, the industry has professionalized significantly. Modern private capital comes from institutional-grade firms that prioritize your project's profitability. This creates a genuine partnership mindset. If you don't make money on the flip, the lender's collateral is at risk. They don't want to manage your construction site or take your property. They want a successful exit so they can fund your next project. It's a relationship built on mutual growth rather than institutional gatekeeping. For investors seeking this level of professional support in the Australian property market, The Home Loan Partners provides personalized financial guidance to help navigate complex market dynamics.

Transparency is the hallmark of a reputable lender. Unlike the "loan sharks" of fiction, professional private hard money lenders operate under clear, legally binding contracts. In 2026, new regulations like the FinCEN Residential Real Estate Rule, which became effective March 1, 2026, have further increased oversight. These rules require lenders to maintain strict AML and KYC policies. This means you're working with registered businesses that have verifiable track records. Their success is tied directly to yours, making the process collaborative rather than combative.

Houston's real estate market moves fast. To secure a property in a competitive neighborhood, you must act like a cash buyer. Traditional banks are built to say "no" to distressed properties because their underwriting focuses on your personal income and credit history. Asset-based lending flips the script. It focuses on the property's potential and the After-Repair Value (ARV). By funding rehabs and bridge deals, private capital directly fuels the local housing inventory. You get the speed you need to close in 3 to 5 days, while the bank is still reviewing your tax returns from three years ago.

Many investors believe they are sidelined from the 2026 market because of a less than perfect credit score. This is a significant misconception. Traditional banks view you through the lens of your past financial mistakes. In contrast, private hard money lenders view you through the lens of your future profits. If you have a solid deal on the table, your FICO score becomes a secondary detail rather than a deal-breaker. Understanding what is a hard money loan means realizing that the property itself does the heavy lifting for your qualification.

This "deal-first" approach allows you to move with the speed of a cash buyer. While a bank might spend weeks dissecting your tax returns, an asset-based lender is busy analyzing the property's potential. They want to know if the house can support the debt. If the numbers work, the loan works. It's a pragmatic way to fund real estate that prioritizes current opportunity over historical data. You can analyze your deal's potential using professional tools to see exactly how a lender will view your next project.

In the world of private capital, the asset is the star of the show. The "asset-backed" philosophy means the loan is secured primarily by the real estate itself. A strong deal with plenty of equity can easily mitigate a borrower's past credit hiccups. The most critical metric in this evaluation is the After Repair Value (ARV). Simply put, the After Repair Value (ARV) represents the estimated market value of a property once all planned renovations and improvements are completed. Lenders use this number to determine how much they can safely lend while ensuring you have enough profit margin to succeed.

To understand the level of detail required for a successful high-end flip, you can explore Whole Home Renovations and learn how professional contractors execute full-scale property transformations.

If credit isn't the priority, what is? Private hard money lenders look for a clear, realistic Scope of Work (SOW). They want to see that you understand the costs and timelines associated with the rehab. A proven track record of successful flips is often more valuable to a lender than a 750 FICO score. Experience breeds confidence. If you're a new investor, don't worry. You can bridge the "experience gap" by partnering with a professional lender who offers mentorship and guidance. To further develop your skills in larger property types, you can learn more about Multifamily Schooled and access training for apartment and commercial real estate. These resources provide the guardrails to help ensure your first deal is a profitable one, focusing on the viability of the project rather than just your bank statement.

Many investors walk away from profitable deals because they see a double-digit interest rate and panic. This is a tactical mistake. When you work with private hard money lenders, you aren't just buying money; you're buying speed and capacity. The "expensive" tag is a myth that ignores the most critical factor in real estate: opportunity cost. If a bank takes 45 days to approve a loan, the property is already gone. In the fast-moving 2026 market, the cost of waiting is often 100% of your potential profit.

Compare the math of a short-term loan to a traditional mortgage. A 30-year mortgage at 6% interest results in you paying for the house nearly twice over. A 12% interest rate on a 6-month flip is a fraction of that total cost. You only pay for the time you use the capital. This efficiency allows you to use leverage to scale your business. Instead of sinking all your liquidity into one property, you can use private capital to fund three deals simultaneously. Your return on equity is significantly higher because you're using the lender's money to generate your wealth.

The principle of using external capital to scale is also applicable in the financial markets; TradeFundrr offers access to funded accounts, allowing investors to trade with significantly higher volumes and potentially increase their market returns.

Points are simply origination fees paid at closing. In 2026, the industry standard typically ranges from 1.5 to 3 points. While this is an upfront cost, it's often the price of admission for a 3-to-5-day closing timeline. Most private hard money lenders also utilize interest-only payments. This structure is ideal for rehab projects because it keeps your monthly overhead low while you focus on construction. Imagine finding a $200,000 fix-and-flip in a prime Houston neighborhood. By the time a traditional bank finishes their first round of paperwork, a private lender has already funded your deal, allowing you to beat out cash buyers who can't move as fast as your leveraged offer.

Stop focusing on the interest rate and start focusing on the net profit. A 12% or 15% loan on a deal that nets you $50,000 is infinitely better than a 0% loan on a deal you never closed. Successful investors treat the cost of capital as a simple line item in their business plan, no different than the cost of lumber or labor. It's a necessary expense to produce a finished product. To get a clear picture of your potential returns, use an investment property calculator to run your numbers. Seeing the actual dollar amount of the interest versus your projected profit often makes the decision to use private capital an easy one. When the deal is strong, the percentage is just a detail.

Don't assume every lender has your back just because they have capital. A common mistake is believing all private hard money lenders offer the same level of reliability. In reality, the gap between a seasoned local partner and a "shadow lender" can be the difference between a closed deal and a lost deposit. Shadow lenders are often just brokers in disguise. They don't have their own funds; they simply shop your deal to other people, adding layers of fees and weeks of delays to your timeline. You need a direct source that understands the nuances of hard money loans texas to stay competitive.

Vetting your partner is about more than just comparing interest rates. It's about ensuring they have the liquidity to fund your draws on time and the expertise to value your project accurately. An out-of-state lender sitting in an office three time zones away won't understand why a property in the Houston Heights commands a different premium than one in Sugar Land. They rely on generic algorithms while a local partner relies on boots-on-the-ground data. Before you sign anything, partner with a local Houston lender who can provide a verified Proof of Funds (POF) that sellers actually respect.

Watch out for lenders who demand high upfront fees before they even issue a term sheet. This is a classic red flag. Another major myth involves "100% financing" claims. While these ads are everywhere in 2026, they often come with hidden strings. Usually, 100% financing requires you to cross-collateralize other properties you own, or it only covers the purchase price while leaving you to fund the entire rehab out of pocket. Always ask for a clear breakdown of the total cash to close. If a lender can't give you a straight answer, they aren't the partner you need.

Texas is a unique environment for real estate. Local lenders understand neighborhood-specific ARV trends and can spot a "bad" block that an algorithm might miss. They also bring a network of vetted contractors and inspectors to the table, which is invaluable for first-time flippers. Beyond the property itself, legal knowledge is key. Texas-specific lending laws, such as the state's relatively efficient non-judicial foreclosure timelines, allow local lenders to offer more flexible loan structures because their risk is managed according to local statutes. This expertise ensures your loan is compliant and your exit strategy is realistic for the Houston market.

While securing capital is the first step in scaling, protecting your business infrastructure is the next logical progression for any serious investor. To ensure your firm is built on a secure foundation, you can explore Managed IT and Physical Security Services for professional technical and site protection.

Success in real estate isn't a solo journey. The ultimate goal for reputable private hard money lenders is to see you exit your loan successfully. If you win, we win. At Jet Lending, we've spent over 20 years refining a mentor approach that prioritizes your education alongside your funding. We don't just hand over a check. We provide the tools and expertise to help you navigate your first flip or bridge deal with total confidence. You aren't just a loan number to us; you're a partner in the Houston market.

Let's debunk one final myth: the fear that you'll lose your property if you're one day late on a payment. This fear keeps many talented investors on the sidelines. Real life happens. Renovation delays and permit hold-ups are part of the business. Professional lenders prefer communication over foreclosure. We offer extensions and work with you to keep the project on track. Our interest is in your successful exit, not in owning your collateral. We want you to finish the project, sell for a profit, and come back to us for your next deal.

We've streamlined our process to match the energetic pulse of the industry. It starts with a focus on results and ends with you at the closing table. Our workflow is designed to be efficient, purposeful, and entirely transparent.

Don't wait for a perfect bank approval that may never arrive. Traditional institutions aren't built for the agility required in 2026. They're built to say no to the very deals that create wealth. Build your capital stack today by partnering with private hard money lenders who value your growth. To further diversify your funding options, Koval Investments provides 0% interest solutions and credit repair services that allow you to maximize your leverage. Contact Jet Lending for a comprehensive deal review and see how our asset-backed focus can fuel your portfolio. Real estate wealth is built on speed and smart leverage. Take the first step toward your next successful closing and start scaling your business with a partner you can trust.

Success in the 2026 real estate market requires more than just finding a great property. It requires the right capital partner. By partnering with the right private hard money lenders, you prioritize your profit margins over your personal credit score. You've learned that focusing on the After-Repair Value rather than outdated financial history provides the leverage needed to close more deals in less time. Speed isn't just a luxury; it's the competitive edge that allows you to beat out cash buyers and institutional competitors.

Don't let the myths of the past hold your business back. You now understand that the true cost of capital is a small price to pay for the ability to scale. With over 20 years of Texas lending experience, we provide the local Houston expertise and transparent, asset-based underwriting you need to succeed. Ready to fund your next Houston deal? Get a fast quote from Jet Lending today. Your next big opportunity is waiting. Grab it with a partner who is as invested in your exit strategy as you are.

Yes, they are legal and regulated for business-purpose investment loans. In Texas, these lenders focus on non-owner-occupied properties, which makes them exempt from many consumer-focused mortgage regulations. Professional private hard money lenders must still comply with state-level licensing and federal anti-money laundering rules, such as the FinCEN requirements implemented in March 2026. This ensures a transparent and legal framework for your real estate investments.

You typically need a down payment of 30% to 35% of the property value. Most lenders offer a maximum Loan-to-Value (LTV) ratio between 65% and 70% to manage their risk. Some specialized programs might allow for a lower down payment if the property has a high After-Repair Value (ARV). This "skin in the game" ensures that both you and the lender are committed to a successful exit.

Yes, you can qualify because the loan is primarily based on the asset's value. While a traditional bank would likely reject a 500 FICO score immediately, private hard money lenders prioritize the profitability of the deal. If the property's After-Repair Value (ARV) is strong and your Scope of Work is realistic, your personal credit history becomes a secondary factor in the approval process.

While real estate investors focus on large-scale asset-based funding, individuals with smaller, immediate financial requirements often look for similar flexibility in the personal loan market. To understand how brokers assist in these scenarios, you can discover Pixie Loans and explore their approach to connecting consumers with lenders for short-term personal needs.

Most local lenders can close a deal in 3 to 5 business days. This speed is a massive advantage compared to the 30 to 45 days required for conventional bank mortgages. Local Houston experts can move quickly through underwriting because they understand neighborhood-specific trends and don't get bogged down in institutional bureaucracy. This efficiency allows you to secure properties in competitive markets where cash buyers usually dominate.

The main difference lies in the level of professional structure and capital sources. Private money lenders are often individual investors lending their personal cash, which can lead to inconsistent terms or availability. Hard money lenders are typically professional firms with established processes, consistent liquidity, and institutional-grade underwriting. Both provide asset-based capital, but hard money firms usually offer more reliability and faster closing timelines for serious investors.

Most professional lenders require an appraisal to verify the property's current and future value. However, they often use specialized investor appraisals that focus heavily on the After-Repair Value (ARV) rather than just comparable sales. Professional firms such as JSRE Sàrl highlight the importance of accurate property estimation and valuation in ensuring that every real estate transaction is backed by sound data. Some local lenders may use a Broker Price Opinion (BPO) or internal valuation tools to speed up the process. This step protects both parties by ensuring the property can support the debt.

You should contact your lender immediately to request a loan extension. Most lenders prefer to extend the term rather than pursue foreclosure because they want to see you succeed and exit the loan profitably. As long as you show clear progress on the renovation and maintain open communication, extensions are a common part of the business. Expect to pay an extension fee to cover the additional time.

Many short-term hard money loans do not have prepayment penalties. Since these loans are designed for quick fix-and-flip projects, lenders expect you to pay off the balance within 6 to 12 months. However, some contracts may include a "minimum interest" clause, which ensures the lender earns a baseline return even if you sell the property in record time. Always review your term sheet for these specific details before closing.

Tags:

Why are you still waiting 45 days for a bank approval while your competitors close deals in less than a week? You know that in the fast-paced 2026 Texas market, speed is often the only difference...

Imagine you just found a high-margin off-market deal in Houston, but the seller demands a closing within ten days or they're moving to the next buyer. You know that traditional banks will spend weeks...

Your credit score shouldn't be the thing that stands between you and a profitable real estate deal. Most investors are tired of waiting months for a traditional bank to say "no" because of a rigid...